Top Quant Stock Pick This Week – July 2, 2026

7th Weekly Top Stock Pick is revealed

Selection for this week

Some Pros about the stock

Some Cons about the stock

Criteria for choosing

The previous selections

Micron Technology has been a favorite on the Quantitative research platform that I follow for some time now. The recent earnings report has caused the EPS rating to move into the top range and now Micron qualifies to be selected Top Stock of the Week. Micron is the top rated stock in the Quant system currently.

Add: MU (Micron Technology) – Semiconductors

What does the company do?

Micron Technology, Inc. (NASDAQ: MU) develops and manufactures memory and storage solutions, including DRAM, NAND flash, high-bandwidth memory (HBM), and SSDs. Its products serve AI data centers, PCs, smartphones, networking, automotive, industrial, and consumer markets worldwide under the Micron and Crucial brands. Founded in 1978, Micron is headquartered in Boise, Idaho.

Why Some Investors Are Bullish

Micron is the only U.S.-headquartered manufacturer of HBM chips — an irreplaceable bottleneck in the world’s largest infrastructure build.

Only three companies globally manufacture HBM at scale, and Micron is the only U.S.-based supplier.

Massive AI spending by hyperscalers is creating unprecedented demand and giving Micron pricing power unlike anything in its history.

• HBM capacity is fully sold out through year-end with multi-year contracts locking in revenue visibility.

HBM supply is fully booked and HBM4 shipments are ramping rapidly.

Long-term agreements provide revenue visibility that is uncommon for a historically cyclical memory company.

• Gross margins have reached levels the memory industry has never seen before.

Revenue and margins have surged as AI memory has become a scarce, mission-critical component.

Tight supply and advanced packaging constraints continue to support exceptional profitability.

• The forward valuation is shockingly cheap relative to near-term earnings growth.

Despite explosive growth and repeated earnings beats, Micron trades at a relatively low forward earnings multiple.

The valuation reflects investor skepticism about how long the AI-driven upcycle can last.

• Analyst consensus is overwhelmingly bullish with price targets implying significant additional upside.

The vast majority of analysts rate the stock a Buy or Strong Buy.

Wall Street broadly believes the AI memory supercycle still has significant runway.

What Bears Are Worried About

The memory industry is brutally cyclical and Samsung and SK Hynix are expanding aggressively.

Every prior memory boom eventually ended with oversupply and collapsing margins.

The key question is whether AI demand remains strong enough to absorb the coming capacity additions.

• $100 billion in fab commitments creates massive financial risk if the cycle turns before the investment pays off.

Memory manufacturing is extremely capital intensive and difficult to scale back quickly.

If AI spending slows, Micron could face falling revenue while still carrying enormous fixed investment obligations.

• The options market and put/call positioning signal meaningful near-term downside risk at current price levels.

Options pricing suggests investors are preparing for significant volatility around earnings and guidance.

Institutional traders continue to actively hedge against a potential downside surprise.

Bottom Line

Micron’s investment thesis has fundamentally improved thanks to AI-driven HBM demand and stronger pricing power, but investors must balance the enormous growth opportunity against the industry’s long history of boom-and-bust cycles and the risks that come with large-scale capacity expansion.

Top Quant Stock of the Week Criteria

I am using a Quantitative research platform that provides a daily list of top-ranked stocks to buy or sell, based on a Comprehensive Quant Score. This Quant system uses computer algorithms to come up with its rankings. This score incorporates multiple factors, including valuation, growth, profitability, momentum, and EPS revisions.

I will be giving heavy weight to strong momentum and strong EPS revisions to make the weekly selection. Then, I will use my tested proprietary criteria to sort and then break any tie.

One stock will be selected each week. That would make 52 selections a year if I don’t miss any weeks because of internet problems.

The hold times for the stocks added will be 1 week to years. Although a 1 week hold would be rare, it could happen if the stocks Quant metrics took a big nose dive right after being selected. If an added stock maintains its good metrics, it will be kept in the portfolio until it doesn’t. No time limit. The Quant system will tell me when it is time to let it go. So the hold time is short, medium and long depending on the Quant system metrics.

All countries are included. ADR’s are ok but Pink Sheet stocks will not be allowed.

Certain Industries are excluded. My testing shows they do not perform well using Quantitative rankings. Two of the main ones are BioTechnology and Pharmacueticals.

The Remove Criteria: Once the stock no longer qualifies to be retained in the Portfolio, it will be removed. This could be because the companies metrics have deteriorated since selection, it is involved in a buyout or financial reporting problems.

Once a stock has been added to the Active list, it will not be added to. No doubling down.

The stocks considered are larger small cap, mid cap, large cap and Mega cap. They will be fairly easy to trade with opening or closing market orders as one of the ways to enter and exit positions.

It should be expected that about 50 stocks will be Active in the Portfolio in any given week, once it gets to the two year mark.

All stocks are added as equal weight. No rebalancing is to occur.

To be considered for addition, the stock has to be in the top group of Quant rankings for just several weeks. This is to allow newly upgraded stocks to qualify quickly. Hopefully, this will catch a couple of strong momentum stocks early in their move.

Once a stock is removed for cause, it can be added back in once it meets the add criteria. No waiting period is required.

There will be no limits on percentages of stocks in the Portfolio by Sector or Industry.

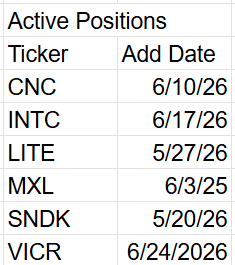

Previous Selections:

For a look at the live scorecard for Position Trader, see the google doc link below.

It has the Live performance numbers and some links back to more information about the three Quant stock Model Portfolio's.

https://live-scorecard.position-trader.com/